Cathie Wood is the head of Ark Investment Management, which operates a family of exchange-traded funds (ETFs) focused on innovative technology stocks. Last year, Wood said software companies could be the next big opportunity in the artificial intelligence (AI) industry. She predicts they will eventually generate $8 in revenue for every $1 they spend on AI data center chips from suppliers like Nvidia.

And Wood has put her money where her mouth is. Since making that call, she has piled into AI software companies like xAI, Anthropic, and OpenAI through the private Ark Venture Fund. Plus, Ark’s ETFs hold several AI software stocks, including Tesla, Palantir, Meta Platforms, and Microsoft.

If Wood is ultimately right about AI software companies, here’s why Google parent Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL) could be among the biggest winners.

Alphabet is transforming Google Search using AI

Alphabet is a tech conglomerate that is home to Google, YouTube, self-driving vehicle company Waymo, and a host of other businesses. Google Search accounted for more than half of Alphabet’s $84.7 billion in revenue during the second quarter of 2024, driven by its 90% market share in the internet search industry. But that dominance faces its greatest-ever test because of AI.

AI chatbots, like OpenAI’s ChatGPT, provide direct responses to users’ queries, giving them rapid access to information on almost any topic. Google, on the other hand, requires users to sift through web pages to find the information they need and generates revenue by charging businesses money to promote their websites in the search results. As a result, the traditional search model is very important for Alphabet.

But rather than defend what could eventually become obsolete, Alphabet decided to make drastic changes. In many cases, users who run Google Search queries will now receive AI-generated, text-based responses above the web search results to give them faster access to information. Google also launched AI Overviews earlier this year, taking that concept a step further.

Overviews incorporate text, images, and links to third-party websites to provide more complete answers to prompts within Search. Plus, with the click of a button, the user can simplify or break down responses to gain a better understanding of the content. Alphabet has already discovered that links within Overviews receive more clicks compared to the same links in the traditional search format, so this new feature could be a big driver of advertising revenue in the future.

On top of that, Alphabet now offers its own family of AI models called Gemini (and a chatbot with the same name), which can answer complex questions and generate content like text and images. For an additional fee, Gemini is already available as an add-on in Google Workspace, which is home to productivity apps such as Gmail, Docs, Sheets, and more. As a result, it could become a powerful driver of subscription-based revenue over time.

Google Cloud is Alphabet’s fastest-growing business

Search might be Alphabet’s largest business, but Google Cloud is growing at twice the pace. It generated a record $10.3 billion in revenue during the 2024 second quarter, a 29% increase from the year-ago period — compared to 13.7% growth in Search.

Google Cloud provides a portfolio of services to help businesses succeed in the digital age, such as data storage, web hosting, and software development tools, among others. However, the platform has also become a leading provider of AI services.

Developers can access the computing power they need to create AI software through Google Cloud’s data centers. To accelerate their progress, they can even use the latest ready-made large language models (LLMs). That includes Gemini and over 130 others from leading start-ups and third-party developers.

Google Cloud is also designing its own data center chips to give AI software developers more choices, which helps differentiate the platform from other cloud providers that rely primarily on suppliers like Nvidia. Google recently launched its sixth-generation tensor processing unit (TPU) called Trillium, which achieves almost five times the peak computing performance of the previous generation.

Most AI developers pay for computing capacity by the minute, so faster chips can substantially reduce costs. Plus, circling back to Wood’s forecast, if Google makes its own chips at scale, the payoff could be significantly larger when it uses them to create software — or leases them to other developers — because it won’t have to send billions of dollars to suppliers like Nvidia.

Alphabet stock is cheap, but there is one big caveat

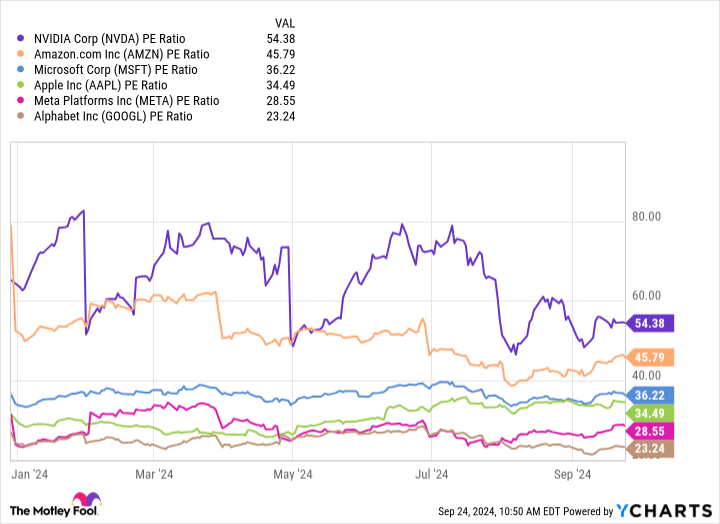

Alphabet generated $6.97 in earnings per share during the past four quarters, and based on its stock price of $161.85 as of this writing, it trades at a price-to-earnings (P/E) ratio of 23.2. That makes Alphabet the cheapest of all the U.S. technology companies valued at $1 trillion or more:

But there is one glaring problem, and it has nothing to do with the company’s growth or its position as an AI powerhouse.

The U.S. Department of Justice (DOJ) filed an antitrust lawsuit against Alphabet in 2020, alleging the company engaged in monopolistic practices by paying Apple as much as $20 billion a year to make Google the default search engine on its devices. Unfortunately for Alphabet, the judge in the case handed down a decision last month and sided with the DOJ.

It’s unclear what the consequences will be. Alphabet might have to pay a financial penalty, or the government could force a breakup of the entire company. The latter would create significant uncertainty for investors because Alphabet would likely have to sell certain parts of its business to satisfy the DOJ that it won’t engage in anti-competitive behavior in the future.

Many Wall Street analysts say a breakup would be an extreme and unlikely outcome. Technology analyst Dan Ives of Wedbush Securities thinks Alphabet will reach a settlement with the DOJ within the next 18 months to bring the matter to a close. That could involve a financial penalty and some changes to how Alphabet structures deals with its partners.

Absent a settlement, it could take years to reach a final resolution while Alphabet appeals the judge’s decision, so the status-quo should prevail for now. Therefore, Alphabet stock looks like a great value at the current price, and if the company does emerge from this regulatory situation intact, it could look like an absolute bargain, considering Cathie Wood’s AI software forecast.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $756,882!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 23, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Palantir Technologies, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Cathie Wood Says Software Is the Next Big AI Opportunity — 1 Spectacular Stock You’ll Regret Not Buying if She’s Right was originally published by The Motley Fool